How the Establishment of Great British Railways Represents the Biggest Rail Restructuring Since Privatisation

![]() Posted on February 7, 2026

Posted on February 7, 2026

![]() Reading time: 13

minutes.

Reading time: 13

minutes.

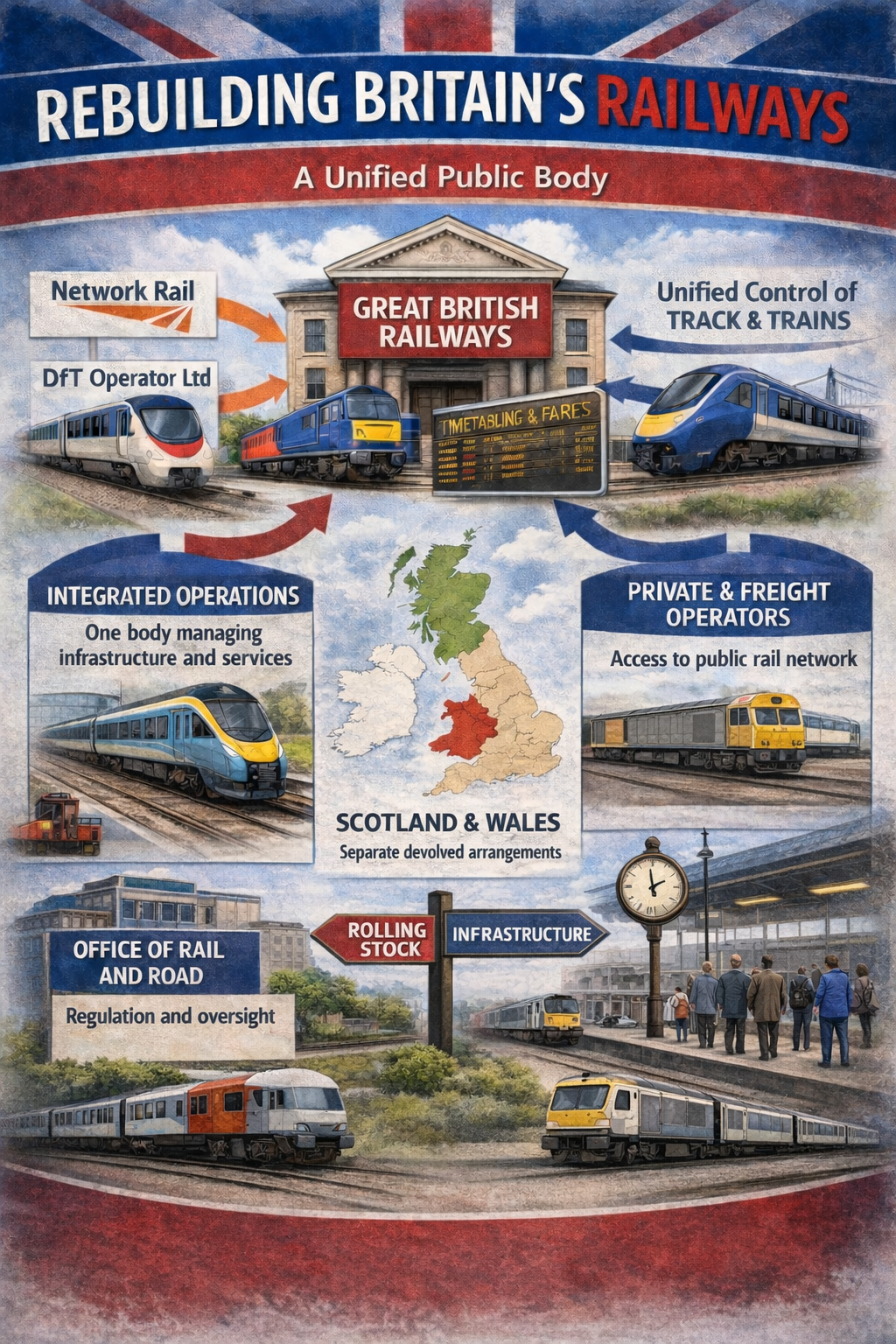

The creation of Great British Railways represents the most fundamental restructuring of Britain’s railway since privatisation in the 1990s. GBR is intended to unify functions that have been split across organisations since privatisation, bringing together infrastructure, timetable planning and fares alongside the contracted passenger railway. Where DfT Operator Ltd exists as a temporary holding structure for nationalised operators, Great British Railways is designed to be permanent, absorbing Network Rail, DfT Operator Ltd and key functions from the Department for Transport into a single public body responsible for running Britain’s railway.

The establishment of GBR has been a long time coming. Plans were first announced in 2021 under the previous Conservative government, following the Williams-Shapps Review which called for radical reform of the fragmented railway system. However, progress stalled, and by 2024 little had been achieved beyond the creation of a shadow organisation. The election of the Labour government in July 2024 gave the project renewed momentum, with the Passenger Railway Services (Public Ownership) Act 2024 receiving Royal Assent in November and a Railways Bill introduced to Parliament in November 2025. This legislation, once it becomes law, will formally establish Great British Railways and set out its powers and responsibilities.

GBR is expected to be fully operational during the 2027 to 2028 period, depending on the timing of legislation and implementation. The government has promised to base the organisation outside London to promote economic growth and skills in a region outside the capital. In February 2022, the Department for Transport launched a public consultation for the location of GBR’s headquarters, though a final decision has not yet been announced. Laura Shoaf chairs the shadow Great British Railways, preparing for the organisation’s formal establishment.

The GBR Model: Reunifying Track and Train

At the heart of the GBR model is the reunification of track and train. Since privatisation, the railway has been split between infrastructure management (Network Rail) and passenger operations (train operating companies), with coordination handled through contracts, access agreements and regulatory oversight. This separation has been widely criticised for creating fragmentation, misaligned incentives and operational inefficiencies. Delays caused by infrastructure problems become the train operator’s responsibility for compensation purposes, even though the operator has no control over the track. Timetable planning requires coordination between multiple organisations with different commercial interests. Investment decisions on infrastructure and rolling stock are often made separately, leading to mismatches and missed opportunities.

GBR is designed to solve these problems by bringing track and train under unified management. It will absorb Network Rail’s functions, becoming the infrastructure owner and manager for most of Great Britain. This means GBR will own and maintain the track, signalling, stations and other fixed assets, employing the engineers, signallers and infrastructure staff who keep the physical railway running. At the same time, GBR will absorb the train operating companies currently held by DfT Operator Ltd, bringing passenger services under the same organisational roof. Staff who currently work for LNER, Northern, South Western Railway and the rest will become GBR employees, operating trains under what is expected to be a unified brand.

This unified structure is intended to create a single point of accountability. When a train is delayed, GBR will be responsible for both the infrastructure that caused the delay and the service affected by it. When timetables are planned or investment is considered, the same organisation will make decisions about track capacity and train operations, infrastructure and rolling stock together rather than in isolation. The ambition is to create what the government calls a “directing mind” for the railway, an organisation with the authority and capability to manage the system as a coherent whole.

Timetabling, fares and ticketing will also be brought under GBR’s control. Currently, timetable planning involves negotiations between train operators, Network Rail and the Department for Transport, with the Rail Delivery Group coordinating industry-wide ticketing and some commercial activities. Under GBR, timetabling will become an internal planning exercise rather than a negotiation between separate organisations, potentially allowing for more efficient use of capacity and better integration between services. Fares policy and ticketing systems will also be managed centrally, with the potential for simpler fare structures and more integrated ticketing, though this will depend on political decisions about pricing and subsidy.

The Rail Delivery Group, which has coordinated some industry-wide functions under the current fragmented model, will be absorbed into GBR, along with relevant parts of the Department for Transport that currently manage contracts with train operators. This consolidation is intended to reduce duplication and streamline decision-making, concentrating railway management expertise within a single organisation rather than spreading it across multiple bodies.

Devolution Within GBR

While GBR is intended to be a Great Britain-wide organisation, devolution means that Scotland and Wales will have different relationships with it than England. Infrastructure ownership and strategic control do not map neatly onto each other, and the model for GBR has been designed to accommodate the constitutional realities of devolution while maintaining a single infrastructure owner.

In Scotland, the likely model under GBR mirrors the current arrangement with Network Rail. Infrastructure will be legally owned by GBR, but strategic control will remain devolved. Scottish Ministers, working through Transport Scotland, will specify funding, investment priorities and performance requirements, and GBR Scotland will function as a distinct business unit shaped by those requirements. This maintains the substance of devolution while avoiding the complexity and cost of splitting infrastructure ownership along the England-Scotland border.

The practical effect is that GBR Scotland will operate day-to-day infrastructure management under strategic direction from the Scottish Government, while train services in Scotland will continue to be run by ScotRail, which is owned by the Scottish Government and will not be absorbed into GBR. Caledonian Sleeper, also owned by the Scottish Government, will similarly remain separate. GBR’s role in Scotland will therefore be limited to infrastructure, with passenger services remaining under Scottish control. Coordination between GBR and the Scottish Government will be necessary for cross-border services and for managing the interface between infrastructure and operations, but the expectation is that this will be handled through established mechanisms rather than requiring major institutional innovation.

In Wales, infrastructure devolution has been more limited. Most rail infrastructure in Wales is owned and managed by Network Rail, with control largely retained by the UK Department for Transport. Welsh Government’s main lever is over train services through Transport for Wales Rail, which has been in public ownership since February 2021 and will not be absorbed into GBR. Under the GBR model, most infrastructure in Wales would be expected to be owned and operated by GBR, while Welsh Government continues to control Transport for Wales Rail services.

A notable exception is the Core Valleys Lines around Cardiff, which were transferred fully to Welsh Government ownership in 2020, creating a pocket of infrastructure that sits outside the main Network Rail ownership model. These lines are expected to remain under Welsh Government ownership under GBR, meaning there will be a small part of the Welsh rail network where both infrastructure and services are devolved. For the rest of Wales, GBR would own and operate infrastructure while Welsh Government controls train services, requiring coordination between the two organisations for timetabling, investment and operational matters.

England is the most straightforward case. GBR is expected to bring together infrastructure and most passenger operations along with timetable and ticketing responsibilities, creating a fully integrated model where track and train are managed by the same organisation. There are no devolution considerations in England, and the expectation is that GBR will exercise direct control over both infrastructure and operations, subject to funding and policy direction from the UK government.

What Stays Outside GBR

Not every part of Britain’s railway will be absorbed into Great British Railways. Open access passenger operators and the freight sector are expected to remain in private ownership, operating as commercial businesses on GBR-managed infrastructure.

Open access passenger operators such as Lumo, Hull Trains and Grand Central operate outside the contracted system entirely. They are private companies that run services on the national network without government contracts and without operating subsidy, taking commercial risk and relying on ticket revenue. Lumo, owned by FirstGroup, began running low-cost services between London King’s Cross and Edinburgh in 2021, offering a budget alternative to LNER’s contracted services on the same route. Hull Trains, also owned by FirstGroup, has operated between London King’s Cross and Hull since 2000. Grand Central, owned by Arriva Group, has run services since 2007, linking London with Sunderland and Bradford.

These operators pay track access charges to use the network and fit into the timetable through an approvals process that considers capacity, performance impacts and the effect on publicly funded services. Under GBR, the expectation is that they will continue to exist as private businesses, with GBR acting as the infrastructure owner and timetable coordinator. The Office of Rail and Road will remain central to regulating access and preventing unfair discrimination, ensuring that GBR as infrastructure manager does not favour its own train services over open access operators or create barriers to market entry.

The government has indicated that open access operators will continue to have a role where they “add value and capacity to the network”, suggesting that the policy is to maintain competition on routes where it can operate without undermining publicly funded services. The regulatory framework will be crucial here, as GBR will be both the infrastructure manager and the dominant passenger operator, creating potential conflicts of interest that the ORR will need to manage.

Freight sits even more clearly outside the passenger ownership debate. Britain’s rail freight sector has been fully privatised since the 1990s and is expected to remain so under GBR. Freight operators pay access charges to use the network and continue to run commercially, carrying goods ranging from intermodal containers and aggregates to automotive parts and specialist loads. The main companies include DB Cargo UK, owned by Deutsche Bahn, Freightliner owned by Brookfield Asset Management, GB Railfreight owned by Infracapital and Colas Rail UK owned by the Colas Group. Direct Rail Services is a notable exception in ownership terms, being owned by the UK Nuclear Decommissioning Authority, but it remains separate from GBR and operates specialist traffic including nuclear material as well as other freight and support services.

Under a GBR model, freight operators will continue to run trains while GBR manages the infrastructure, allocates capacity and coordinates timetables. The government has indicated that GBR will have a statutory duty to promote rail freight, including a rail freight growth target, recognising the sector’s importance for decarbonisation and for moving goods efficiently. This is intended to ensure that freight is not squeezed out as GBR prioritises its own passenger services, though the practical balance between passenger and freight access will depend on capacity constraints, operational priorities and regulatory oversight.

Rolling stock ownership is another area that will remain outside GBR. The trains themselves are owned by rolling stock leasing companies (ROSCO’s), private firms that purchase trains and lease them to operators. This arrangement has continued throughout privatisation and is expected to continue under GBR. The government has indicated that nationalising the ROSCO’s would be prohibitively expensive, and that leasing provides flexibility for operators to adjust their fleets as demand changes. GBR will therefore lease trains from ROSCO’s rather than owning them outright, maintaining a significant role for private capital in the railway even as passenger operations and infrastructure are brought into public ownership.

Managing a Mixed Railway

The challenge for GBR will be managing a railway where infrastructure and most passenger services are publicly owned, but where private operators continue to run some passenger services and all freight. This requires a framework for allocating track capacity, planning timetables and resolving disputes that balance public service obligations with the access rights of commercial operators.

Track access rights are the foundation of this framework. Contracted passenger services operated by GBR will form the core of the timetable because they are tied to public service obligations and detailed specifications about frequency, calling patterns and service quality. These services are the reason the infrastructure exists in its current form, and they carry the vast majority of passengers. Freight operators also have firm access rights reflecting their economic role and their importance for decarbonisation, though their paths are often planned around peak passenger periods where possible due to the operational constraints created by slower trains with different performance characteristics.

Open access passenger services have access rights too, but these are more conditional and must be approved with regard to network capacity and impacts on public service operations. The approvals process considers whether an open access service would abstract revenue from publicly funded services (the “not primarily abstractive” test) and whether it would cause operational problems or require infrastructure investment that would not be justified by the benefits. This means open access operators face higher barriers to entry than they would in a fully commercial market, but the principle remains that access should be available where it does not undermine public service or create unmanageable operational problems.

Timetable construction under GBR will typically proceed in layers, beginning with infrastructure constraints and engineering access (the times when the track needs to be closed for maintenance or renewal), then building core passenger service patterns, then integrating freight paths and finally fitting open access services where capacity allows. This hierarchy reflects policy priorities, with publicly funded passenger services and infrastructure maintenance taking precedence, followed by freight (which has statutory protection) and then commercial passenger services.

Disputes over access are shaped by contractual rights and regulatory oversight, with the Office of Rail and Road providing a safeguard to ensure decisions are not arbitrary and that competition and freight needs are protected even where the infrastructure manager is closely linked to the dominant passenger operator. The ORR has powers to investigate complaints, require changes to access arrangements and impose penalties for anticompetitive behaviour. This regulatory backstop is crucial for maintaining confidence in the system, particularly for freight operators and open access passenger operators who will be dealing with an infrastructure manager that is also their competitor.

The ORR will also have broader responsibilities under GBR, including setting the framework for infrastructure funding through five-year control periods (similar to the current model with Network Rail), monitoring performance and efficiency, and ensuring that investment decisions are justified and well-managed. This provides a degree of independent oversight over GBR’s infrastructure activities, reducing the risk that political pressures or operational short-termism lead to underinvestment or poor decision-making.

Integration and Permanence

Great British Railways represents a fundamental shift in how Britain’s railway is organised. Where privatisation created fragmentation and DfT Operator Ltd has provided a temporary holding structure for nationalised operators, GBR is designed to be a permanent, integrated organisation responsible for both infrastructure and passenger operations. The ambition is to create a railway that works as a coherent system rather than a collection of separate businesses, with unified planning, clear accountability and the ability to make long-term decisions about investment and service development.

The success of GBR will depend on how effectively it manages the tensions inherent in its structure. It must balance public service obligations with commercial efficiency, accommodate devolution while maintaining a unified infrastructure, and provide access for private operators while prioritising publicly funded services. It must deliver better performance and value for money than the current fragmented system, while avoiding the pitfalls that led to the decline of British Rail before privatisation.

The result will be a railway that may look familiar to passengers in many respects, with trains running on the same routes and serving the same stations, but with a fundamentally different organisational structure behind the scenes. Track and train will be managed by the same organisation for the first time in three decades, with the potential for better integration, clearer accountability and more coherent long-term planning. At the same time, devolved operators in Scotland and Wales will remain outside GBR’s passenger operations, and privately run open access and freight operators will continue to operate on the network, creating a mixed model that reflects both the political realities of devolution and the practical need to maintain competitive access for non-GBR operators.

Whether this model delivers the improvements promised by its advocates will become clear over the coming years as GBR takes shape and begins to reshape Britain’s railway.

Recent Musings

Getting Around Canada Without a Car

From Navan to Belfast, Irish Rail Improvements Continue to Take Shape

How Iarnród Éireann's Investment Programme Is Reshaping the Rail Network Across Ireland

Integrated Rural Transport Coming to Derbyshire

Extras & Utilities

Carrying Bicycles on Buses in Britain and Ireland

Not Just Blogs, A Collection of Public Transport News Sources